Credit and Debit Card Payments in Pakistan 2026;Why Digital Shopping Still Faces Barriers

Credit and debit card payments in Pakistan are becoming increasingly popular. People now prefer to use debit cards, credit cards, mobile banking applications, QR codes and digital wallets for shopping, restaurant bills, fuel purchases, hotel payments and online transactions.

Digital payment is safer than carrying cash, creates a record of payment and can help consumers prove a transaction when a shopkeeper refuses to issue an invoice, delivers defective goods or denies receiving payment. However, despite this growing public demand, credit and debit card payments in Pakistan are still not accepted widely in many markets.

Large shops, restaurants, hotels, bakeries, tailors, workshops, petrol pumps and branded outlets often refuse card payments. In other cases, businesses accept a card only after demanding an additional 2% or 2.5% charge from the customer. This practice discourages documented transactions and pushes the public back towards cash.

Credit and Debit Card Payments in Pakistan Are a Public Need

Pakistan cannot develop a documented and modern economy while major commercial businesses continue to rely mainly on cash. Credit and debit card payments in Pakistan should no longer be treated as a luxury facility available only at selected stores.

Every major business should provide at least one convenient electronic payment method, including:

- Debit and credit card POS machines;

- Raast QR-code payments;

- Mobile wallet payments;

- Online payment links;

- Bank-transfer facilities; and

- Soft POS systems through mobile devices.

Electronic payment creates transparency. It helps customers retain proof of payment and makes it more difficult for businesses to hide sales, understate turnover or avoid issuing proper invoices.

FBR’s Point of Sale framework is designed to improve documentation and invoice reporting by qualifying retailers. Businesses and consumers should understand the importance of FBR POS legal provisions and properly documented sales.

Why Credit and Debit Card Payments in Pakistan Are Still Refused

One of the biggest problems with credit and debit card payments in Pakistan is refusal by merchants. A customer may have sufficient balance in a bank account and a valid debit or credit card, yet the shopkeeper may insist on cash.

This is especially common in local markets, restaurants, workshops, petrol pumps, clothing stores, pharmacies and service businesses. Some businesses have enough turnover to install a POS terminal but choose not to do so because cash sales are easier to keep outside formal records.

Cash-only transactions can create several problems:

- Customers may not receive a proper invoice;

- Businesses may understate actual sales;

- Tax authorities may lose visibility over commercial activity;

- Consumers may face difficulty proving payment later; and

- Digitalisation and financial inclusion remain weak.

Pakistan’s tax policy should reward transparency, not allow documented consumers to be inconvenienced for choosing lawful payment methods.

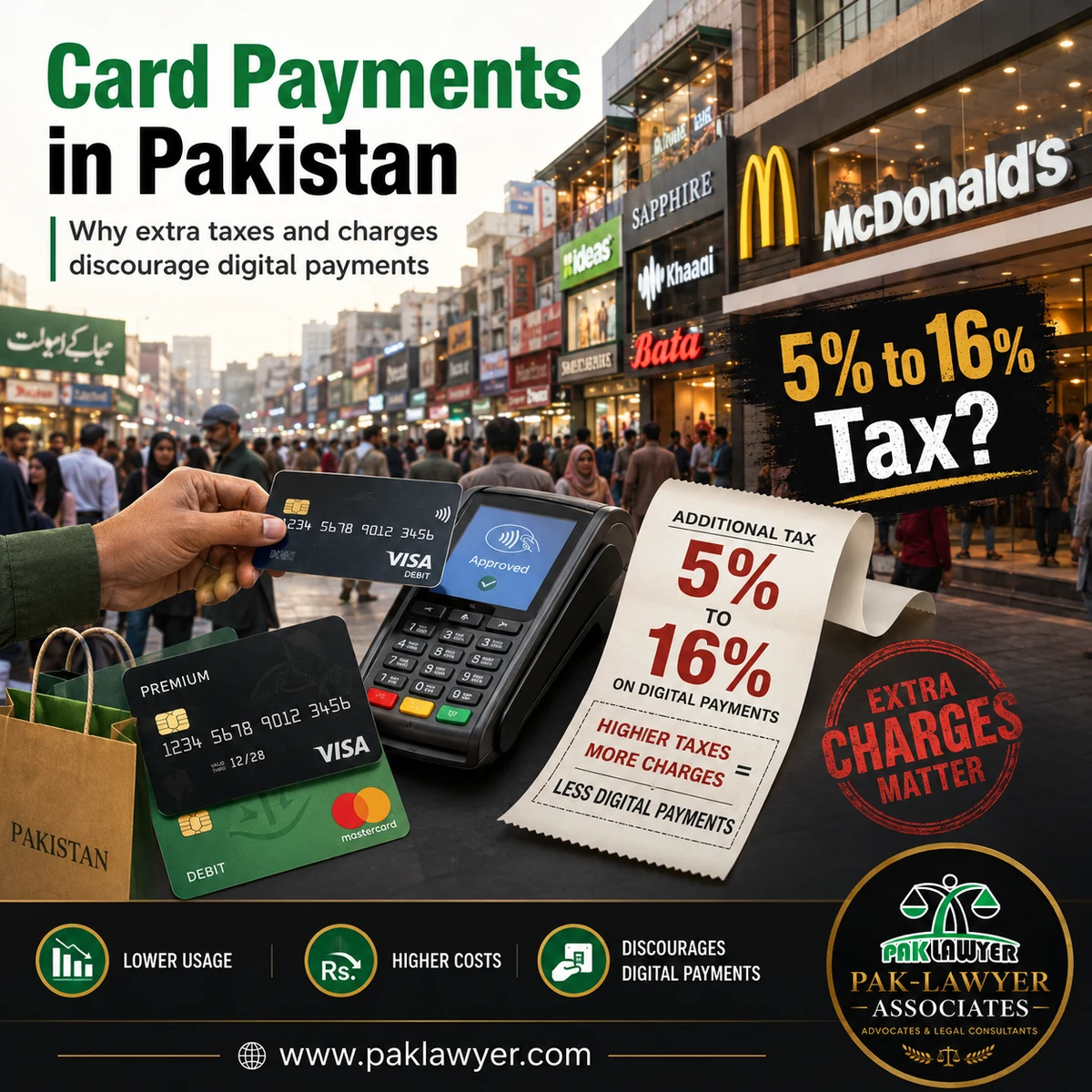

The 2.5% Card Charge Is Often MDR, Not a Government Tax

Many customers are told that they must pay an extra 2% or 2.5% because they are using a debit or credit card. This amount is frequently described as a “card tax.” In many cases, however, the charge relates to the Merchant Discount Rate, commonly called MDR.

MDR is generally a payment-processing cost paid by a merchant to the acquiring bank or payment service provider. It is not automatically a government tax charged directly to the consumer. The State Bank of Pakistan’s card-acceptance circular discusses the payment-card framework and MDR structure for domestic POS transactions.

Therefore, businesses should not mislead customers by calling every card-related cost a “government tax.” Where a merchant applies any additional charge, it must be clearly disclosed before payment and separately reflected on the invoice.

More importantly, merchants should explore lower-cost alternatives such as Raast QR payments. Under the Raast Person-to-Merchant payment framework, customers should not be charged a fee for making purchases through Raast P2M.

Credit and Debit Card Payments in Pakistan and Restaurant Tax

The tax treatment of restaurant bills has become a major public concern. Customers often notice different tax rates, service charges, delivery charges, packaging charges and other amounts added to their final bill.

In Punjab, restaurant tax can differ according to the mode of payment. The law has provided a lower rate for payment through debit cards, credit cards, mobile wallets and QR scanning, while other payment modes may attract a higher rate. Consumers should always check the applicable notification and invoice because tax rules can change through finance legislation and provincial notifications.

Reports regarding the Punjab Finance Bill 2026 indicated a proposal to increase the reduced restaurant rate on digital payments from 5% to 8%, while retaining a higher rate for other payment methods. This creates a policy concern: if the government wants people to use cards and digital methods, the tax advantage for documented transactions should remain meaningful.

Credit and debit card payments in Pakistan should be encouraged through lower friction, transparent billing and convenient acceptance—not through additional confusion at the checkout counter.

McDonald’s, KFC and Other Restaurant Chains: Need for Transparent Invoices

Multinational and large restaurant chains, including McDonald’s, KFC and other branded outlets, should ensure complete invoice transparency. Customers frequently question why a restaurant invoice may show 16% tax along with service charges, delivery charges, packaging charges or other additions.

The existence of a tax or service charge does not automatically mean that it is unlawful. The legal issue is whether every amount is correctly applied, properly disclosed and supported by the relevant provincial tax regime or contractual terms.

Restaurants should clearly separate the following on every invoice:

- Sales tax;

- Service charge, where applicable;

- Delivery or packaging charges;

- Discounts offered on digital payments;

- Any optional gratuity or voluntary amount; and

- The final amount payable by cash, card or QR payment.

The Punjab Revenue Authority should ensure that customers can understand the legal basis of each charge. Consumers may consult the Punjab Revenue Authority FAQs and retain invoices whenever they believe tax has been incorrectly calculated.

FBR, SBP and Provincial Authorities Must Improve Enforcement

If FBR and provincial authorities genuinely want to increase tax collection, they must focus on bringing more businesses into the documented economy. Merely increasing rates on already visible and documented transactions cannot solve the wider problem.

FBR should strengthen POS integration and invoice verification, especially for large retailers and restaurants. The official FBR POS integrated retailers database shows that electronic documentation is already expanding, but the country still needs much wider merchant coverage.

The government should introduce a practical policy requiring medium and large businesses to offer at least one electronic payment method. Small businesses should be supported through low-cost Raast QR codes, subsidised POS devices and easy merchant onboarding.

What Authorities Should Do for Credit and Debit Card Payments in Pakistan

- Require major retailers, restaurants, hotels, petrol pumps and service providers to accept electronic payments;

- Promote Raast QR payments as a low-cost alternative for small businesses;

- Take action against misleading “card tax” claims;

- Require clear and itemised invoices for taxes and service charges;

- Link qualifying business transactions with POS and tax documentation systems;

- Create a public complaint mechanism for refusal to issue invoices or accept digital payments; and

- Keep digital-payment tax rates lower than cash-payment rates to encourage documented transactions.

Consumer Rights When a Shop Refuses Card Payment

Consumers should insist on a proper invoice, especially when paying a significant amount for goods or services. Before making payment, customers should ask whether a debit card, credit card or Raast QR payment is accepted and whether any additional charge applies.

Where a merchant demands an unexplained card charge, the consumer should request that it be shown separately on the receipt. Consumers should also save screenshots, payment alerts, invoices and bank transaction records in case of a dispute.

Digital payments also require basic cyber security. Customers should never share a card PIN, OTP, CVV number or banking password with a shopkeeper or delivery rider. For legal guidance in cases of online scams, fake transactions, identity theft or financial fraud, read our Cyber Crime and Online Financial Fraud Services in Pakistan.

Credit and Debit Card Payments in Pakistan Must Be Encouraged, Not Penalised

Credit and debit card payments in Pakistan can help create a transparent, documented and consumer-friendly economy. They reduce dependence on cash, support better invoicing and help tax authorities identify genuine commercial activity.

However, the policy will fail if businesses continue refusing cards, passing hidden processing costs to customers or presenting MDR as a government tax. Likewise, higher tax rates on digital restaurant payments can weaken the public incentive to choose documented channels.

The better solution is simple: every major market, shop, restaurant, hotel, petrol pump, workshop and service provider should offer a convenient digital-payment option. Government departments should combine strict enforcement with low-cost merchant solutions and transparent tax rules.

Pakistan’s wider digitalisation challenge is not limited to payments. Similar issues arise when public systems become digital without practical access for all citizens. Read our analysis on the Punjab e-Stamp OTP System and public-access concerns.

FAQs About Credit and Debit Card Payments in Pakistan

Can a shop charge extra for using a debit or credit card in Pakistan?

A merchant may claim that it faces payment-processing costs, but the customer should not be misled by describing every additional amount as a government tax. Ask for a clear invoice showing the exact basis of the charge.

Is the 2.5% card charge a government tax?

Not necessarily. In many cases, it is related to MDR or payment-processing cost charged to the merchant by the bank or payment service provider. It should not automatically be presented as a statutory tax payable by the customer.

Why should businesses accept credit and debit card payments in Pakistan?

Credit and debit card payments in Pakistan help create documented transactions, give customers proof of payment, improve tax transparency and reduce the risks associated with cash-only business activity.

What should I do if a restaurant invoice contains unclear tax or service charges?

Ask for an itemised invoice, retain a copy of the bill and verify the applicable provincial tax treatment. Where needed, seek advice from a tax professional, consumer-rights body or legal adviser.

Pak-Lawyer Associates

Advocates & Legal Consultants

Phone: +92 321 4610092

Website: www.paklawyer.com